Second, use the file of residuals, go to the npar (nonparametric statistics) module, and do the runs test. A significant result indicates that the residuals are correlated

>USE

"D:\mydocs\ys209\divorce.syd"

SYSTAT

Rectangular file D:\mydocs\ys209\divorce.syd,

created

Wed Apr 19, 2000 at 00:25:57, contains variables:

YEAR

DIVPOP DIVMF

UNEMP FLFPRT

MARUMF

TREND

First do the regression and save the residuals (repeat).

>mglh

>select

year <= 1970

>model

divmf=constant+unemp+flfprt+marumf

>save

divres01/data

>estimate

Data

for the following results were selected according to:

year <= 1970

Dep

Var: DIVMF N: 51 Multiple R: 0.866237

Squared multiple R: 0.750366

Adjusted

squared multiple R: 0.734432 Standard error of estimate: 1.206846

Effect

Coefficient Std Error Std Coef

Tolerance t P(2 Tail)

CONSTANT

-9.243243 2.117510 0.000000

. -4.36515 0.00007

UNEMP

0.047519 0.035985 0.125499

0.588047 1.32052 0.19306

FLFPRT

0.239771 0.029453 0.672784

0.777664 8.14082 0.00000

MARUMF

0.137210 0.019332 0.606853

0.726515 7.09745 0.00000

Analysis of Variance

Source

Sum-of-Squares df Mean-Square

F-ratio P

Regression

205.764749 3 68.588250

47.091854 0.000000

Residual

68.454466 47 1.456478

***

WARNING ***

Case

26 is an outlier (Studentized

Residual = 3.239025)

Case

27 has large leverage (Leverage = 0.347000)

Case

27 is an outlier (Studentized

Residual = 3.955823)

Durbin-Watson

D Statistic 0.429

First

Order Autocorrelation 0.711

Residuals

have been saved.

-------------------------------------------------------------------------------

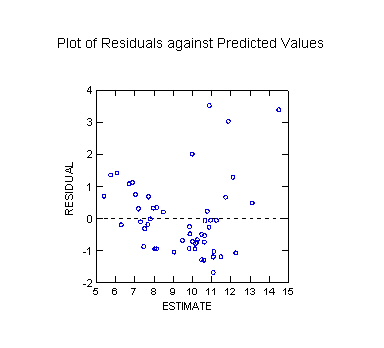

Plot of Residuals against Predicted Values

Second,

use the file of residuals, go to the npar (nonparametric statistics) module,

and do the runs test. A significant result indicates that the residuals

are correlated

>use divres01

SYSTAT

Rectangular file d:\mydocs\ys209\divres01.SYD,

created

Wed Apr 26, 2000 at 13:29:59, contains variables:

ESTIMATE

RESIDUAL LEVERAGE COOK

STUDENT SEPRED

YEAR

DIVPOP DIVMF

UNEMP FLFPRT

MARUMF

TREND

>npar

>runs

residual

Wald-Wolfowitz

runs test using cutpoint = 0.000

Probability

Variable

Cases LE Cut Cases GT Cut Runs

Z

(2-tail)

RESIDUAL

32 19

8 -5.103269

0.000000

Thus one concludes that the residuals in this case are correlated.