SOCI709 (formerly 209) - Module 3 - Diagnostics & Remedies in Simple

Regression

1. Residual Analysis & the Healthy Regression

1. Residual Plot of the Healthy Regression

Residual analysis is a set of diagnostic methods for investigating

the appropriateness of a regression model based on the residuals

ei = Yi - ^Yi

where ^Yi is the fitted value (aka predictor, aka estimate)

^Yi = b0 + b1Xi

The basic idea is that, if the regression model is appropriate, the residuals

ei should "reflect the properties ascribed to the model error

terms ei", such as independence,

constant variance for different levels of X and normal distribution.

The workhorse of residual analysis is the

residual plot, or plot

of the residuals ei against the fitted values

^Yi = b0 + b1Xi.

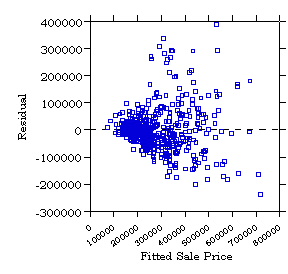

In a healthy regression the residuals should appear as arranged randomly

in a horizontal band around the Y = 0 line, like so

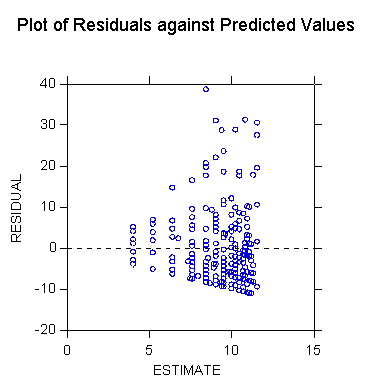

In reality, computer programs typically adapt the range of the data

to occupy the entire frame of the plot, so that the residuals appear as

a random cloud of points spread out over the entire vertical range of the

plot. The next exhibit shows a typical computer-generated residual

plot

2. Potential Problems With the Simple Regression Model

Problems with the regression are departures from ( or violations of)

the assumptions of the regression model. They are:

-

Regression function is not linear

-

Error terms do not have constant variance

-

Error terms are not independent

-

Model fits all but one or a few outlier observations

-

Error terms are not normally distributed

-

One or several important predictor variables have been omitted from model

These problems also affect multiple regression models. Most of the

diagnostic tools used for simple linear regression are also used with multiple

regression.

This module examines these potential problems in conjunction with diagnostic

tools which can be informal (such as graphs) or formal (such

as tests), and remedies.

3. Using Informal (Graphic) Versus Formal Diagnostic Tests

Features of informal graphic diagnostics are

-

they are visual and at least in part subjective

-

they may be inconclusive

-

they require judgment, and therefore

-

they may require training and/or experience

-

sometimes judgment may be helped by calibration (see normal probability

plot, later)

Features of formal tests are

-

they may give a straight yes/no answer about presence of a problem

-

they may not require experience or training

-

they may be used in automatic fashion

-

they may not reveal the substantive situation as well as informal tools,

so that

-

researcher relying entirely on formal tools may miss an interesting aspect

of the data (e.g., in Box-Cox estimation of optimal transformation of the

data)

Researchers can use available informal and formal diagnostics to develop

their own strategy to diagnose problems with their models.

2. Regression Function is Not Linear

1. Scatterplot or Residual Plot With LOWESS Robust Nonparametric

Regression Curve (Diagnostic, Informal)

Nonlinearity in the regression function may appear in the scatter plot

of Y versus X, or in the residual plot. The residual plot often magnifies

nonlinearity (compared to the scatter plot) and makes it more noticeable.

A nonlinear trend may be revealed by using a nonparametric regression

technique such as LOWESS. The LOWESS algorithm estimates a curve

that represents the main trend in the data, without assuming a specific

mathematical relationship between Y and X. (This is why it is called

nonparametric.)

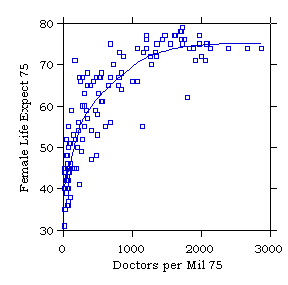

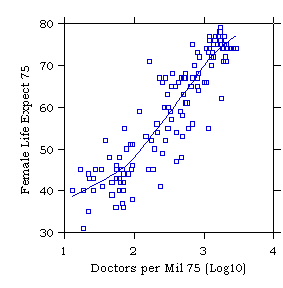

The next two exhibits show (1) a scatterplot of female life expectancy

against doctors per million for 137 countries in 1975, and (2) a plot of

the residuals of the regression of female life expectancy on doctors

per million. Note how the nonlinearity is magnified by the residual

plot, as compared to the plot of Y against X.

LOWESS (aka LOESS) was invented by William S. Cleveland (1994:168-180,

1993:94-101).

2. Linearity or Lack of Fit Test (Diagnostic, Formal, Limited Applicability)

There is a test of linearity of the regression function, called the lack

of fit test. This test requires repeat observations (called replications)

at one or more levels of X, so it cannot be performed with all data sets.

In essence it is a test of whether the means of Y for the groups of replicates

are significantly different from the fitted value ^Y on the regression

line, using a kind of F test. The test is explained in ALSM5e pp.

119-127; ALSM4e pp. 115-124.

3. Polynomial Regression (Remedy)

Some forms of non-linearity can be modeled by introducing higher powers

of X in the regression equation. Polynomial regression is a form

of multiple regression and is discussed in Module 6 - Polynomial Regression

& Interactions.

4. Transforming Variables To Linearize the Relationship (Remedy)

1. Error Variance Appears Constant

When the error variance appears to be constant, only X needs be

transformed to linearize the relationship. Some typical situations

are shown in the next exhibit.

The following exhibit shows an example of a non-linear regression function

that can be straightened by transforming X.

2. Error Variance Appears Not Constant

When the error variance does not appear constant it may be necessary

to transform Y or both X and Y. The next two exhibits show examples.

3. Transformation to Simultaneously Linearize the Relationship and

Normalize the Distribution of Errors

See Box-Cox transformation under 6.2 below.

3. Error Terms Do Not Have Constant Variance (Heteroskedasticity)

1. Funnel-Shape in in Residual Plot (Diagnostic, Informal)

Terminology:

homoskedasticity: s2

is

constant over the entire range of X (as specified by OLS assumptions)

heteroskedasticity: s2

is not constant over the entire range of X (departure from OLS assumptions)

The regression model assumes homoskedasticity. Heteroskedasticity

may be manifested by a funnel or megaphone pattern like the following prototype

A real example is

Sometimes the funnel pattern is reversed, with greater error variance corresponding

to smaller values of X.

Q - Why is the variance in depression score lower for higher incomes and

vice-versa?

However, when the residual is plotted against ^Y the megaphone pattern

fans out to the right. (Why?)

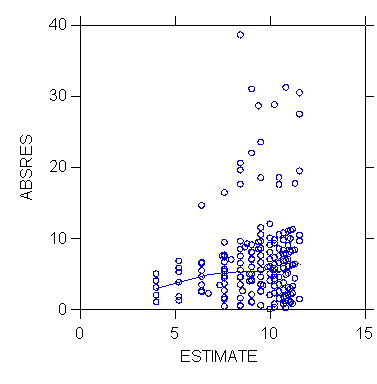

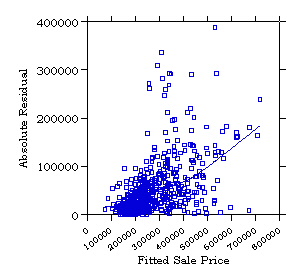

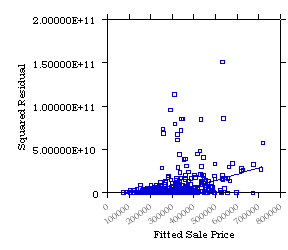

2. Plot of Absolute Residual |e| or Squared Residual e2

by ^Y (Diagnostic, Informal)

A pattern of heteroskedasticity can be detected informally by plotting

the absolute residual or the squared residual against ^Yi; adding

the linear fit or a LOWESS curve helps seeing the trend in the data:

3. Tests for Homoskedasticity (Constancy of s2

) (Diagnostic, Formal)

There are many tests of heteroskedasticity. Three formal tests of

constancy of the error variance will be discussed in Module 12 - Heteroskedasticity

& Weighted Least Squares:

-

the Brown-Forsythe Test (see ALSM5e pp. 116-118; not in ALSM4e)

-

the Breusch-Pagan aka Cook-Weisberg Test (see ALSM5e pp. 118-119;

ALSM4e p. 115)

-

the Goldfeld-Quandt test (Wilkinson, Blank, and Gruber 1996:274-277)

(The Breusch-Pagan aka Cook-Weisberg Test can be carried out in

STATA with the command hettest following the regress command.

An example will be shown in the hands-on session.)

4. Variable Transformation To Equalize the Variance of Y (Remedy)

See Section 6 below on Tukey's ladder of powers and the Box-Cox transformation.

Transformations of Y to make the distribution of residuals normal often

have the effect of also equalizing the variance of Y over the entire range

of X.

5. Weighted Least Squares (Remedy)

In rare cases where a variable transformation that takes care of unequal

error variance cannot be found, one can use weighted least squares.

In weighted least squares observations are weighted in inverse proportion

to the variance of the corresponding error term, so that observations with

high variance are downweighted relative to observations with low variance.

Weighted least squares is discussed in Module 12 - Heteroskedasticity &

Weighted Least Squares.

4. Error Terms Are Not Independent

1. Residual e by Time or Other Sequence (Diagnostic, Informal)

In time series data where observations correspond to successive time points,

errors can be autocorrelated or serially correlated.

Such a pattern can be seen in a plot of residuals against the time order

of the observations, as in the following prototype

The following real example shows residuals for a regression of the

divorce rate on female labor force participation (U.S. 1920-1996).

Note the characteristic "machine gun" tracking pattern. The residual

is plotted against the index of a case (corresponding to a year of observation).

Q - What year is the peak divorce residual?

Remedial techniques for lack of independence are discussed in Module

14 - Autocorrelation in Time Series Data.

2. Durbin-Watson Test of Independence (Diagnostic, Formal)

See Module 14 - Autocorrelation in Time Series Data.

5. Model Fits All But One Or A Few Outlier Observations

1. Outliers in Scatterplot or Residual Plot (Diagnostic, Informal)

Outliers may often (but not always) be spotted in a scatterplot or residual

plot.

Outlying observations may affect the estimate of the regression parameters,

as shown in the following exhibit.

Outlying observations may sometimes be identified in a box plot or stem-and-leaf

display of the residuals (see below).

2. Tests for Outlier and Influential Cases (Diagnostic, Formal)

An extensive discussion of outliers and influential cases is provided in

Module 10 - Outlying & Influential Observations.

6. Error Terms Are Not Normally Distributed

Non-normality of errors corresponds to a range of issues with different

degrees of severity. Kurtosis (fat tails) and skewness are more serious

than more minor departures from the normal. These features of the

distribution blend in with the problem of outlying observations.

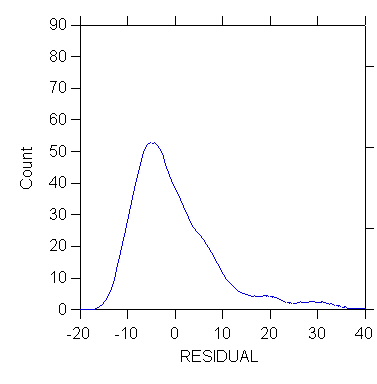

1. Box Plot, Stem-and-Leaf, and Other Displays of the Distribution

of e (Diagnostic, Informal)

Lack of normality (as well as some types of outlying observations) may

be diagnosed by looking at the distribution of the residuals using devices

such as a histogram, stem and leaf display, box plot, kernel density estimator,

etc. In the following examples see how the histogram of the

distribution appears normal but fat tails/outlying observations are revealed

in other displays.

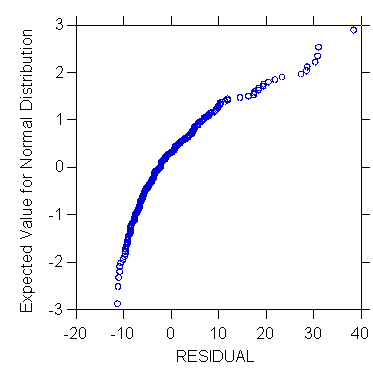

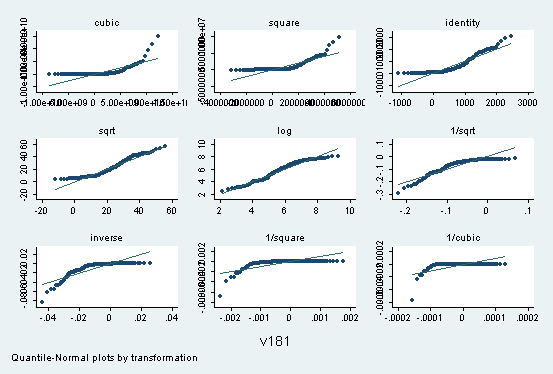

2. Normal Probability Plot of e (Diagnostic, Informal)

The normal probability plot is used to examine whether the residuals are

normally distributed. It is a plot of the residuals against their

expected values assuming normality. The expected values of the residuals

are obtained by first sorting them in increasing order of magnitude.

Then

EXPECTEDk = z((k - 0.5)/n) for k=1,...,n

where k is the rank of the residual such that k = 1 for the smallest value

of e and k = n for the largest, z((k - 0.5)/n) is the 100((k - 0.5)/n)

percentile of the standard normal distribution N(0,1).

When the residuals are normally distributed, the plot is approximately

a straight line.

Notes:

-

the textbook uses an alternative formula for EXPECTEDk that

yields similar results (ALSM5e pp. 110-112; ALSM4e pp. 106-108)

-

especially for relatively small samples, the normal probability plot may

not be conclusive concerning the normality of the distribution. A

formal correlation test (explained later) can be used. Alternatively,

Wilkinson, Blank, and Gruber (1996) suggest calibrating the normal probability

plot by generating probability plots for 10 random samples of size n from

a normal population, and judging visually whether the empirical plot "fits"

within this collection.

-

some computer implementation of the normal probability plot multiply z((k

- 0.5)/n) by the square root of MSE to obtain expected residuals with the

same scale as the original residuals (ALSM5e pp. 110-112; ALSM4e pp. 106-108).

The shape of normal probability plot reveals aspects of the distribution

of e.

The following exhibits show a full example of calculation of the probability

plot based on the Yule data set.

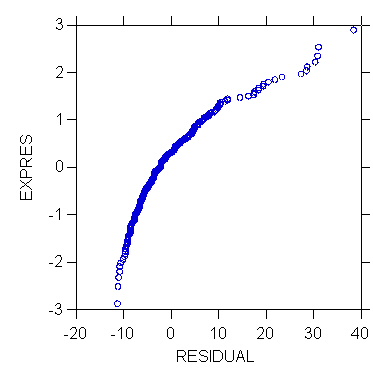

3. Correlation Test for Normality (Diagnostic, Formal)

The correlation test for normality is based on the normal probability plot.

It is the correlation between the residuals ei and their expected

values under normality. The higher the correlation, the straighter

the normal probability plot, and the more likely that the residuals are

normally distributed. The value of the correlation coefficient can

be tested, given the sample size and the a level

chosen, by comparing it with the critical value in Table B.6 in ALSM5e/4e.

A coefficient larger than the critical value supports the conclusion that

the error terms are normally distributed (ALSM5e pp. 115-116; ALSM4e p.

111).

Example: For the Yule data the correlation between residual and value

expected under the normality assumption is .981 with n=32. Table

B.6 in ALSM5e/4e gives the critical values for n = 30 of .964 with

a=.05.

Since r=.981 > .964 one concludes that the residuals are normally distributed.

4. Data Transformations Affecting the Distribution of a Variable

(Remedy)

This section relies extensively on Wilkinson, Blank, and Gruber (1996,

Chapter 22 pp. 695-713).

1. Standardizing a Variable - Does Not Affect Shape of Distribution

Common variable standardizations are the z-score and range standardization.

These transformations do not affect the shape of the distribution of the

variable (contrary to some popular beliefs).

The standardized value Z of Y is obtained by the formula

Z = (Y - Y.) / sY

where Y. and sY denote the sample mean and standard

deviation of Y, respectively.

The range-standardized value W of Y is obtained by the formula

W = (Y - YMIN) / (YMAX - YMIN)

where YMAX and YMIN denote the maximum and minimum

values of Y, respectively.

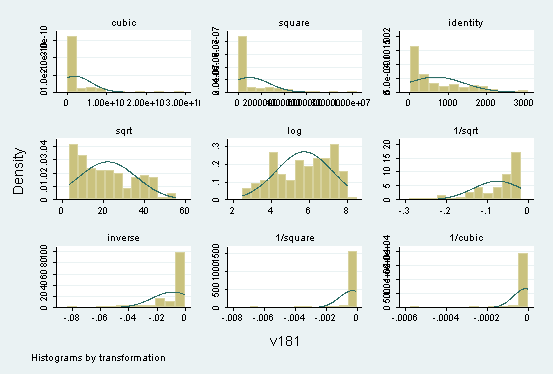

2. Transforming a Variable to Look Normally Distributed

Transformations of Y can be used to remedy non-normality of the error term.

a. Radical normalization with the rankit transformation

The rankit transformation transforms any distribution into a normal one.

It is the same as grading on the curve. It is the same as

finding the expected value of the residual in preparing a normal probability

plot.

b. Tukey's ladder of powers

Tukey (1977) has proposed a ladder of powers spanning a range of

transformations to normalize the distribution of a variable in a data set.

c. Automatic choice of ladder of powers transformation with the Box-Cox

procedure

The family of power transformations in Tukey's ladder is of the form

Y' = Yl

where l is the power parameter. Some of

the principal steps of the ladder are

|

Lambda (l)

|

Transformation |

Name |

|

2

|

Y' = X2 |

square |

|

1

|

Y' = X |

identity |

|

.5

|

Y' = (X)1/2 |

square root |

|

0

|

Y' = log(X) |

logarithm (any base) |

|

-.5

|

Y' = 1/(X)1/2 |

inverse square root |

|

-1

|

Y' = 1/Y |

inverse |

but l can take any value in between.

In the simplest version the Box-Cox procedure estimates the parameter

l

by maximum likelihood so as to maximize the fit of the transformed data

Y' to a normal distribution. There is only one variable involved.

Example: Find the transformation of V181 (female life expectancy) that

best normalizes the distribution. STATA estimates lambda as

| lambda |

Std. Error |

z (same as t*) |

P{|Z|>z} |

CI Low |

CI Up |

Sigma |

| .1362285 |

.0660046 |

2.06 |

.039 |

.0068619 |

.265595 |

3.136496 |

The program does chi-square tests of 3 hypotheses on the value of lambda:

|

H0: l =

|

Chi-square |

P-value |

|

-1

|

300.88 |

.000 |

|

0

|

4.35 |

.037 |

|

1

|

140.35 |

.000 |

So estimated l (.1362285) is close to 0 (logarithm

transformation), but H0: l = 0 is

rejected at the .05 level (although not at the .01 level).

d. Box-Cox procedure to optimize the linear relationship between

X and Y

The Box-Cox procedure can also be used to transform Y and X in such a way

as to maximize their relationship. The procedure can estimate an

exponent

q (theta) of X as well as the exponent

l

(lambda) of Y. The complete model is thus

Yil = b0

+ b1Xiq

+ ei

The estimates l,

b0

, b1 and s2

can be found by maximizing the likelihood function shown in ALSM5e p. 135,

Equation 3.36; ALSM4e p. 135, Equation 3.35. There are now two variables

involved, Y and X. (The model generalizes to multiple regression,

with some limitations.)

In the following example v195 is Female Life Expectancy 1975 and v181

is Doctors per Million 181. The estimates are

| Coefficient |

Coefficient |

Std. Error |

z (same as t*) |

P{|Z|>z} |

95% CI Low |

95% CI Up |

| lambda |

.1772316 |

.0705726 |

2.51 |

0.012 |

.0389119 |

.3155514 |

| theta |

1.422054 |

.3605058 |

3.94 |

0.000 |

.7154761 |

2.128633 |

| V181 |

16.74134 |

Sigma = |

31.67667 |

|

|

|

Note that the exponent theta for X is 1.422, but the 95% CI includes

1.0 so one cannot reject the hypothesis that the optimal theta is 1.0 (optimal

transformation is no transformation).

On the Box-Cox procedure see ALSM5e pp. 134-137.

d. Arcsine transformation for proportions and percents

Proportions and percentages often produce a truncated and skewed distribution

when the mean is not near .5. The arcsine transformation corrects

these problems. Use

let ynew = 2*asn(sqr(P))

where P is a proportion. (Transform percentages to proportions by

dividing by 100 before applying transformation.)

e. Fisher's z transformation for correlation coefficients

Correlation coefficients often produce a truncated and skewed distribution

when the mean is not near 0. Fisher's z transformation (aka hyperbolic

tangent) normalizes such distributions. Use

let ynew = ath(R)

where R is a correlation between -1 and +1.

7. One or Several Important Predictor Variables Have Been Omitted

From Model

Plot of Residual e by Omitted Predictor Variable Z

Z is a potential predictor variable that is not included in the equation.

8. Simple Regression Diagnostics & Remedies in Practice

1. SYSTAT Examples

>USE

"Z:\mydocs\ys209\survey2b.syd"

[...deleted output...]

>regress

>model

total=constant+income

>save

resid/data

>estimate

Dep

Var: TOTAL N: 256 Multiple R: 0.210

Squared multiple R: 0.044

Adjusted

squared multiple R: 0.040 Standard error of estimate: 8.728

Effect

Coefficient Std Error Std Coef

Tolerance t P(2 Tail)

CONSTANT

11.811 0.948

0.000 . 12.461

0.000

INCOME

-0.120 0.035

-0.210 1.000 -3.425

0.001

Analysis

of Variance

Source

Sum-of-Squares df Mean-Square

F-ratio P

Regression

893.479 1 893.479

11.729 0.001

Residual

19348.271 254 76.174

***

WARNING ***

Case

256 is an outlier (Studentized

Residual = 4.598)

Durbin-Watson

D Statistic 0.659

First

Order Autocorrelation 0.631

Residuals

and data have been saved.

>use

resid

SYSTAT

Rectangular file Z:\mydocs\s208\resid.SYD,

created

Mon Jan 20, 2003 at 10:04:34, contains variables:

ESTIMATE

RESIDUAL LEVERAGE COOK

STUDENT SEPRED

ID

SEX AGE

MARITAL EDUCATN

EMPLOY

[...deletd

output...]

>let

absres = abs(residual)

>plot

absres*estimate/stick=out smooth=lowess

>den

residual/stick=out kernel

>pplot

residual/stick=out

>rem

calculate expected residuals under normality explicitly

>rem

to do correlation test

>sort

residual

256 cases and 56 variables processed.

>let

resrank = case

>list

residual resrank/n=10

Case number RESIDUAL

RESRANK

1 -11.212

1.000

2 -11.092

2.000

3 -10.973

3.000

4 -10.733

4.000

5 -10.733

5.000

6 -10.494

6.000

7 -10.015

7.000

8 -9.733

8.000

9 -9.571

9.000

10 -9.536

10.000

>let

expres = zif((resrank - 0.5)/256)

>rem

next plot should be same as pplot command

>plot

expres*residual/stick=out

>corr

>pearson

expres*residual

Pearson

correlation matrix

RESIDUAL

EXPRES

0.926

Number

of observations: 256

>rem

test for normality using correlation test and

>rem

ALSM5e Table B.6

>plot

residual*female/stick=out smooth=linear

>den

income/stick=out kernel

>den

income/stick=out kernel

>rem

the kernel density of income is "normalized" by setting the power

>rem

exponent interactively after double-clicking on the graph, as shown

>rem

in following picture

>rem

this yields the kernel density with power exponent = 0.2

>USE

"Z:\mydocs\ys209\world209.syd"

[...deleted output...]

>plot

v195*v181/stick=out smooth=lowess

>rem scatterplot

with LOWESS curve shows strong non-linear

>rem pattern; relationship

"straightend" by setting power

>rem exponent of

V181 to 0.2 interactively after double-

>rem clicking on

graph

>plot

v195*v181/stick=out smooth=lowess

2. STATA Examples

(By Catherine Harnois and

Cheol-Sung Lee, TAs in Spring 2003.)

We

highly recommend the UCLA STATA module for diagnostics

. use "C:\Stata\auto.dta",

clear

*1978 Automobile Data

. boxcox mpg, nolog

level(95)

Transform: (mpg^L-1)/L

L [95% Conf. Interval]

Log Likelihood

----------------------------------------------------

-0.3584 -1.1296 0.4078

-123.2664

Test: L == -1 chi2(1) =

2.68 Pr>chi2 = 0.1018

L == 0 chi2(1) =

0.82 Pr>chi2 = 0.3649

L == 1 chi2(1) =

12.25 Pr>chi2 = 0.0005

*nolog level(95) tells

Stata not to display the iterations log but to include

a 95% confidnence

interval. The interval rejects the hypothesis that the best

transformation

is no transformation.

*next create a new variable

newmpg based on the optimal exponent found by boxcox procedure

. gen newmpg = (mpg^(-0.3584)

- 1)/(-0.3584)

*next compare distributions

of mpg and newmpg

. graph mpg, bin(10)

ylabel xlabel norm t1(raw data)

.

graph newmpg, bin(10) ylabel xlabel norm t1(transformed data)

.

kdensity mpg, normal border

.

kdensity newmpg, normal border

.

ksm mpg weight, lowess xlab ylab border

.

ksm newmpg weight, lowess xlab ylab border

. stem mpg

Stem-and-leaf plot for

mpg (Mileage (mpg))

1t | 22

1f | 44444455

1s | 66667777

1. | 88888888899999999

2* | 00011111

2t | 22222333

2f | 444455555

2s | 666

2. | 8889

3* | 001

3t |

3f | 455

3s |

3. |

4* | 1

. ladder mpg

Transformation

formula

Chi-sq(2) P(Chi-sq)

------------------------------------------------------------------

cube

mpg^3

43.59 0.000

square

mpg^2

27.03 0.000

raw

mpg

10.95 0.004

square-root

sqrt(mpg)

4.94 0.084

log

log(mpg)

0.87 0.647

reciprocal root

1/sqrt(mpg)

0.20 0.905

reciprocal

1/mpg

2.36 0.307

reciprocal square

1/(mpg^2)

11.99 0.002

reciprocal cube

1/(mpg^3)

24.30 0.000

In this formula, m=mu

and s=the standard deviation and I is the observation number.

.

pnorm mpg

.

pnorm newmpg

. regress mpg weight

Source |

SS df

MS

Number of obs = 74

---------+------------------------------

F( 1, 72) = 134.62

Model |

1591.9902 1 1591.9902

Prob > F = 0.0000

Residual | 851.469256

72 11.8259619

R-squared = 0.6515

---------+------------------------------

Adj R-squared = 0.6467

Total |

2443.45946 73 33.4720474

Root MSE = 3.4389

------------------------------------------------------------------------------

mpg | Coef. Std. Err.

t P>|t| [95%

Conf. Interval]

---------+--------------------------------------------------------------------

weight |

-.0060087 .0005179 -11.603 0.000

-.0070411 -.0049763

_cons |

39.44028 1.614003 24.436

0.000 36.22283 42.65774

------------------------------------------------------------------------------

.

fpredict yhat

.

fpredict e,resid

.

graph e yhat

.

rvfplot, oneway twoway box yline(0) ylabel xlabel

. hettest

Cook-Weisberg test for

heteroscedasticity using fitted values of mpg

Ho: Constant variance

chi2(1) = 11.05

Prob > chi2 = 0.0009

. ovtest

Ramsey RESET test using

powers of the fitted values of mpg

Ho: model has no omitted variables

F(3, 69) = 1.77

Prob > F = 0.1616

Appendix - Mathematical Functions

Mathematical and Satistical Functions Available in SYSTAT

Mathematical and Satistical Functions Available in STATA

Please consult STATA Manual

Last modified 30 Jan 2006

![Exhibit: Female life expectancy by literacy: residual by estimate [m3002.gif]](m3002.gif){kind=link}

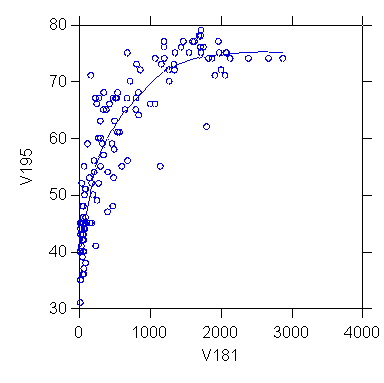

![Exhibit: Plot of female life expectancy against doctors per million ca. 1975, with LOWESS curve (repeat) [m16004.jpg]](m16004.jpg){kind=link}

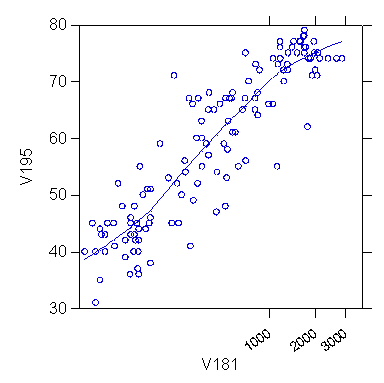

![Exhibit: Residual plot for the regression of female life expectancy against doctors per million ca. 1975, with LOWESS curve [m16005.jpg]](m16005.jpg){kind=link}

![Exhibit: Prototype nonlinear plots with equal error variance (ALSM5e F3.13 p. 130; ALSM4e F3.13 p. 127) [m3009.gif]](m3009.gif){kind=link}

{kind=link}

{kind=link}

![Exhibit: Prototype nonlinear plots with unequal error variance (ALSM5e F3.15 p. 132; ALSM4e F3.15 p. 130) [m3010.gif]](m3010.gif){kind=link}

![Exhibit: Transformations on scatterplots to linearize a relationship (WBG F22.4 p. 705) [m3014.gif]](m3014.gif){kind=link}

{kind=link}

![Exhibit: Plot of TOTAL (depression scale) by INCOME showing greater variance in depression score for smaller income values [m3039.jpg]](m3039.jpg){kind=link}

![Exhibit: Residual plot for regression of TOTAL (depression scale) on INCOME [m3037.jpg]](m3037.jpg){kind=link}

{kind=link}

{kind=link}

![Exhibit: Plot of absolute residuals against estimate for regression of TOTAL (depression scale) on INCOME [m3038.jpg]](m3038.jpg){kind=link}

![Exhibit: Residuals of divorce rate on female labor force participation, by file index (year) -- U.S. 1920-96 [m3054.jpg]](m3054.jpg){kind=link}

![Exhibit: Distorting effect of outlier (ALSM5e F3.7 p. 109; ALSM4e F3.7 p. 104) [m3020.gif]](m3020.gif){kind=link}

![Exhibit: Effect of outlying observation on estimated regression line (NWW Figure 19.9 p. 590) [m16008.gif]](m16008.gif){kind=link}

![Exhibit: Distribution of residuals of regression of female life expectancy on literacy rate (v227) [m16007.jpg]](m16007.jpg){kind=link}

![Exhibit: Stem and leaf plot of residuals [m3021.gif]](m3021.gif){kind=link}

![Exhibit: DOT ("DIT") plot and box plot [m3022.gif]](m3022.gif){kind=link}

![Exhibit: Normal probability plot of residuals of female life expectancy on literacy rate [m3023.gif]](m3023.gif){kind=link}

![Exhibit: Normal probability plots (ALSM5e F3.9 p. 112; ALSM4e F3.9 p. 108) [m3024.gif]](m3024.gif){kind=link}

![Exhibit: Plot of PAUP by OUTRATIO [m3033.gif]](m3033.gif){kind=link}

![Exhibit: Normal probability plot of residuals for the regression of PAUP on OUTRATIO [m3055.jpg]](m3055.jpg){kind=link}

![Exhibit: Standardizing a variable (WBG F22.1 p. 697) [m3011.gif]](m3011.gif){kind=link}

![Exhibit: Normalizing a variable (WBG F22.2 p. 699) [m3012.gif]](m3012.gif){kind=link}

![Exhibit: Ladder of power transformations to normalize a variable (WBG F22.3 p. 703) [m3013.gif]](m3013.gif){kind=link}

{kind=link}

{kind=link}

![Exhibit: Female life expectancy by literacy: residual by other variable [m3025.gif]](m3025.gif){kind=link}

![Exhibit: SYSTAT arithmetic functions (SYSTAT 6.0 Data p. 119) [m3026.gif]](m3026.gif){kind=link}

![Exhibit: SYSTAT distribution functions (SYSTAT 6.0 Data p. 143) [m3027.gif]](m3027.gif){kind=link}