Soci709 (formerly 209) Module 14 - AUTOCORRELATION IN TIME SERIES DATA

Resources:

ALSM5e pp 481--498; ALSM4e pp 497--516

Hamilton 2006 pp. 339-360 (especially commands tsset date and prais y

x1 x2)

1. AUTOCORRELATION OF ERRORS: NATURE OF

THE PROBLEM

Time series data are observed on the same unit

(individual, country, firm, etc.) at n points in time. EX:

-

yearly divorce rate in the U.S. from 1922 to present

-

quarterly profits of a company

-

income inequality in the U.S. measured each year

from 1964 to present

-

daily atmospheric pollen count in Chapel Hill

since first recorded, etc.

In regression models using time series data the

errors are often correlated over time (they are said to be autocorrelated

or serially correlated).

NKNW illustrate the problems caused by correlated

errors with simulated data generated with the model:

-

Yt = b0

+ b1Xt

+ et

-

et = et-1

+ ut

-

Xt represents "time", so that X1=1,

X2=2, etc.

-

b0 = 2;

b1

= .5

-

e0 (et

prior to beginning the process) = 3

The simulated data are shown in the next exhibit.

As seen in the next exhibit, the errors et

are positively correlated.

Because of serial correlation

-

the OLS and true regression lines may differ sharply

from sample to sample depending on the initial disturbance e0

(compare (a), (b) and (c) in next exhibit)

-

MSE may underestimate true variance of et

(compare variability of residuals around regression line in (a) and (b)

in next exhibit); thus standard errors of estimate of the regression coefficients

may also be underestimated

These patterns can be seen in the next exhibit

In general, serial correlation of the disturbances

may have the following effects with OLS estimation

-

estimated regression coefficients are still

unbiased but no longer minimum variance (= inefficient)

-

MSE (the OLS estimate of s2)

may underestimate the true variance of errors

-

s{bk} may underestimate true standard

error of estimate

-

thus, statistical inference using t and F is no

longer justified

2. AUTOCORRELATION DIAGNOSTICS

1. Plot of Residuals Against Time or Sequential

Order

An informal diagnostic of autocorrelation of errors

is to plot the residuals from the OLS regression against time or against

the sequential order of the observation in the file (after checking that

observations are in fact arranged in chronological order!). Connecting

the points with a dotted line makes any pattern of autocorrelation more

conspicuous. Look for evidence of "tracking", in which residuals

corresponding to adjacent time points have similar values. (Some

people say to look for a pattern like that made by bullets fired from a

machine gun.)

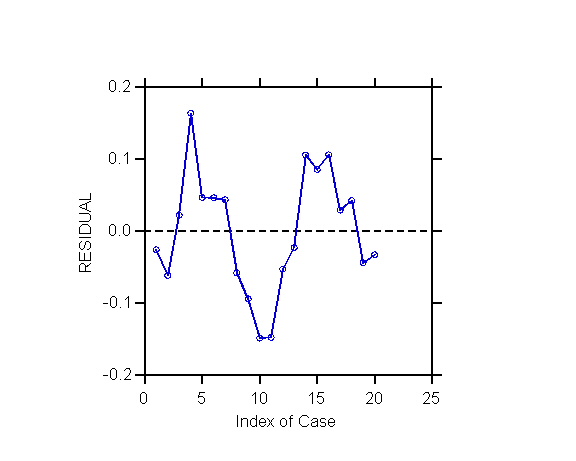

Exhibit: Index plot

(= time plot) of residuals for Blaisdell data

2. The Wald-Wolfowitz Runs Test

The Wald-Wolfowitz runs test is a non-parametric

test that detects serial patterns in a run of numbers. Applied to

the residuals of the OLS regression, a significant test indicates the presence

of sequences of positive or negative residuals longer than expected by

chance alone. Such long sequences of residuals above or below zero

is what one would expect if the errors are "tracking" because of autocorrelation.

For the Blaisdell data the test is significant

(p=.006) so one concludes that the errors are correlated.

3. The Durbin-Watson Test

The Durbin-Watson (D-W) test is the most commonly

used test of autocorrelation of residuals.

The D-W D statistic is calculated from the

ordinary OLS residuals et = Yt - ^Yt as

D = St=2

to n (et - et-1)2 / St=1

to n et2

where n is the number of cases.

To understand the D-W formula consider that

-

when et and et-1 are correlated

they have similar values

-

thus when et and et-1 are

correlated the terms (et - et-1)2 are

small and the numerator of D is small (while the denominator is the same

no matter how much autocorrelation there is)

-

thus small values of D (close to zero) indicate

serial correlation

The D-W test setup is

H0: r

= 0

H1: r

> 0

Table B7 gives critical values dL and

dU such that

if D > dU conclude H0

(r = 0)

if dL <= D <= dU

the test is inconclusive

if D < dL conclude H1

(r > 0)

Example: SYSTAT routinely reports the D-W

D statistic with every regression (D has no meaning unless observations

are sequentially ordered). For the Blaisdell data D = .735.

Table B7 for n=20 and p-1=1 gives dL=.95 and dU=1.15.

Since .735 < .95 = dL one concludes H1 (errors

are autocorrelated).

3. REMEDIAL MEASURES FOR AUTOCORRELATION

1. Add Omitted Predictors to Model

Autocorrelation is caused by unmeasured variables

that have similar values from period to period. Identifying these

variables and including them in the model may eliminate the serial correlation.

Some of these substantive omitted variables may be "simulated" by adding

to the model

-

a linear or exponential trend

-

seasonal indicators

If adding a trend or seasonal indicators gets

rid of the autocorrelation, this is by far the best solution to the problem.

2. The First-Order Autoregressive Error

Model With Generalized Least Squares Estimation

1. First-Order Autoregressive Error Model

The model is

Yt = b0

+ b1Xt1

+ b2Xt2

+ ... + bp-1Xt,p-1

+ et

et =

ret-1

+ ut

where

|r|

< 1 (r

is Greek "rho" and denotes the autocorrelation parameter)

ut is i.i.d. ~ N(0, s2)

One can show the following consequences of model

assumptions (see ALSM4e pp. 501-502; try to express these relationships in

words):

-

E{et}

= 0

-

s2{et}

= s2/(1-r2)

-

s{et,

et-1}

= r(s2/(1-r2))

-

r{et,

et-1}

= s{et,

et-1}/(s{et}s{et-1})

= r

-

r{et,

et-s}

= rs

Thus the variance-covariance matrix of e

is non-diagonal with a specific structure; s2{e}

=

| k |

kr |

kr2 |

... |

krn-1 |

| kr |

k |

kr |

... |

krn-2 |

| ... |

... |

... |

... |

... |

| krn-1 |

krn-2 |

krn-3 |

... |

k |

where

k = s2/(1-r2)

( k is Greek

"kappa")

(This is why the model is called "generalized",

as in "generalized least squares"; see Module 12.)

Even though the first-order autoregressive

model is simple, it is often a good approximation of actual situations.

2. Generalized Least Squares Estimation

Using Transformed Variables

Assume (for the sake of argument) that one knows

the value of r.

Define the transformed variables

Yt' = Yt - rYt-1

Xtk' = Xtk - rXt-1,k

Then one can show that the regression

Yt' = b0'

+ ... + bk'Xtk'

+ ... + ut

based on the transformed variables has error term

ut which is no longer serially correlated, and that bk

= bk'

except that b0'

= b0(1-r)

(see NKNW pp. 508-509). Thus if one knows r

one can get rid of the serial correlation by using OLS with the transformed

data.

(This transformation can be derived from the

application of GLS estimation to the non-diagonal variance-covariance matrix

of e generated

by the autocorrelation. So the transformation is a special case of

GLS estimation.)

In practice the value of r

is unknown. The 3 classical methods of estimation in the presence

of autocorrelation discussed next (Cochrane-Orcutt, Hildreth-Lu, first

differences) are all based on transforming the variables, using alternative

ways of estimating r.

3. Cochrane-Orcutt Procedure

The Cochrane-orcutt procedure is

-

do an OLS regression of Yt on the Xtk

and calculate the residuals et

-

estimate the autocorrelation r

as

r = St=2

to n et-1et / St=2

to n et-12

-

use r to transform the variables into Yt'

and Xtk' using formula above; do an OLS regression of Yt'

on the Xtk'

-

if the D-W test still indicates serial correlation,

reestimate r using residuals computed using the original variables Yt

and Xtk and the regression coefficients estimated from the (last)

transformed regression; go to 3.

The following exhibits show the Cochrane-Orcutt

procedure with the Blaisdell data.

4. Hildreth-Lu Procedure

The Hildreth-Lu procedure searches for the estimate

of r that minimizes

the sum of squared errors of the transformed regression, i.e.

SSE = S(Yt'

- ^Yt')2

(Hilderth-Lu is similar to the Box-Cox procedure

to estimate the parameter l

of a power transformation of Y.)

One can search for the optimal r

by calculating the transformed regression for closely spaced values of

r

and choosing the one with smallest SSE, as shown in NKNW.

One can also estimate r

and the regression coefficients simultaneously using iterative methods

(nonlinear least squares). This can be done using the NONLIN module

of SYSTAT, as shown in the exhibit analyzing the Blaisdell data.

Exhibit: (REPEAT) Replication

of Cochrane-Orcutt, Hildreth-Lu, & first differences procedures for

Blaisdell data

5. First Differences Procedure

First differences is the simplest transformation

procedure as it implicitly assumes r

= 1. This assumption is often approximately justified because

-

estimates of r

are often close to 1

-

the relationship of SSE with r

is often "flat" (as seen in the Hildreth-Lu procedure: see ALSM4e Table 12.5

p. 513) for values of r

near the optimum, so the estimate of r

does not need to be exact

The first differences transformation is thus

Yt' = Yt - Yt-1

Xtk' = Xtk - Xt-1,k

The first differences procedure involves two

regressions with the transformed data:

-

a first regression without a constant term

to estimate the regression coefficients (since the first differences transformation

"wipes out" the constant term)

-

a second regression with a constant term

to recalculate the D-W D statistic only (because the D-W formula requires

a constant in the model)

6. Comparison of the 3 Transformation Methods

Results of the 3 transformation methods (compared

with OLS) are shown in the following table.

Regression results for 4 estimation methods

(SYSTAT) - Blaisdell data (compare with ALSM5e <>, ALSM4e Table 12.7 p. 516 - some figures differ slightly)

|

b1 |

s{b1} |

t-ratio |

r |

MSE |

| Cochrane-Orcutt |

.1738 |

.0029 |

59.42 |

.626 |

.004515 |

| Hildreth-Lu (nonlinear LS) |

.1605 |

.0079 |

20.24 |

.959 |

.004479 |

| First differences |

.1685 |

.0051 |

33.06 |

1.0 |

.004815 |

| OLS |

.1763 |

.0014 |

122.0 |

0.0 |

.007406 |

7. STATA Commands

4. COMPREHENSIVE EXAMPLE: U.S. DIVORCE RATE

1920-1970, 1920-1997

1. SYSTAT Analysis

The following exhibit present examples of the

Cochrane-Orcutt, Hildreth-Lu (using nonlinear least squares), and first

differences methods applied to an analysis of the divorce rate in the U.S.

from 1920 to 1970.

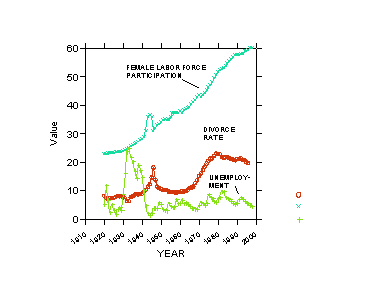

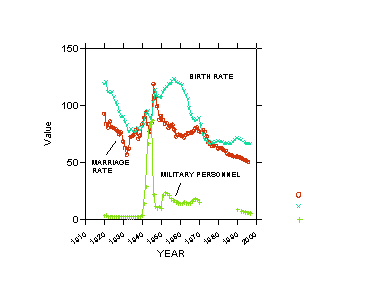

As a substantive epilogue the next 3 exhibits relate to a model of the

divorce rate that is more elaborate than one previously shown, as it includes

a measure of the birth rate (women 15-44) and military personnel per 1,000

population. Only OLS results are shown.

2. STATA Analysis

To be added later.

5. SUMMARY & RECOMMENDATIONS

Analysis of the Blaisdell data and the divorce rates data illustrate the

following approach:

- set up your data as a time-series (i.e., identify variable that

represents time, or the sequential order of observations) is required by

your software (e.g., tsset in STATA)

- do an OLS regression and test for autocorrelation of residuals (using

Wald-Wolfowitz run test and Durbin-Watson test)

- if autocorrelation is significant consider adding to the models

variables that might contribute to the autocorrelation

- do a Prais-Winston regression, two-step and iterated

- if this solution fails investigate more complicated error structures

(beyond this module)

Last modified 24 Apr 2006

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}